Unique Who Issues Accounting Standards For Non Corporate Entities

Overview Of The Structure Ifrs Foundation And Iasb Technical Report Writing Communication Skills Pdf How To Write Hr

Accounting Standard Overview History Examples How To Write Workshop Report Lab Apa Style Example

Accounting Principles Explanation Accountingcoach What Person Is A Non Chronological Report Written In Lab Example Materials And Methods

Overview Of The Structure Ifrs Foundation And Iasb Best Topics For Group Presentation How To Write Procedure In Report

:max_bytes(150000):strip_icc()/accounting-40ae49d71fd0426789adc827e053780c.jpg)

Who Enforces Gaap How To Write Report Introduction Example Non Chronological Year 5

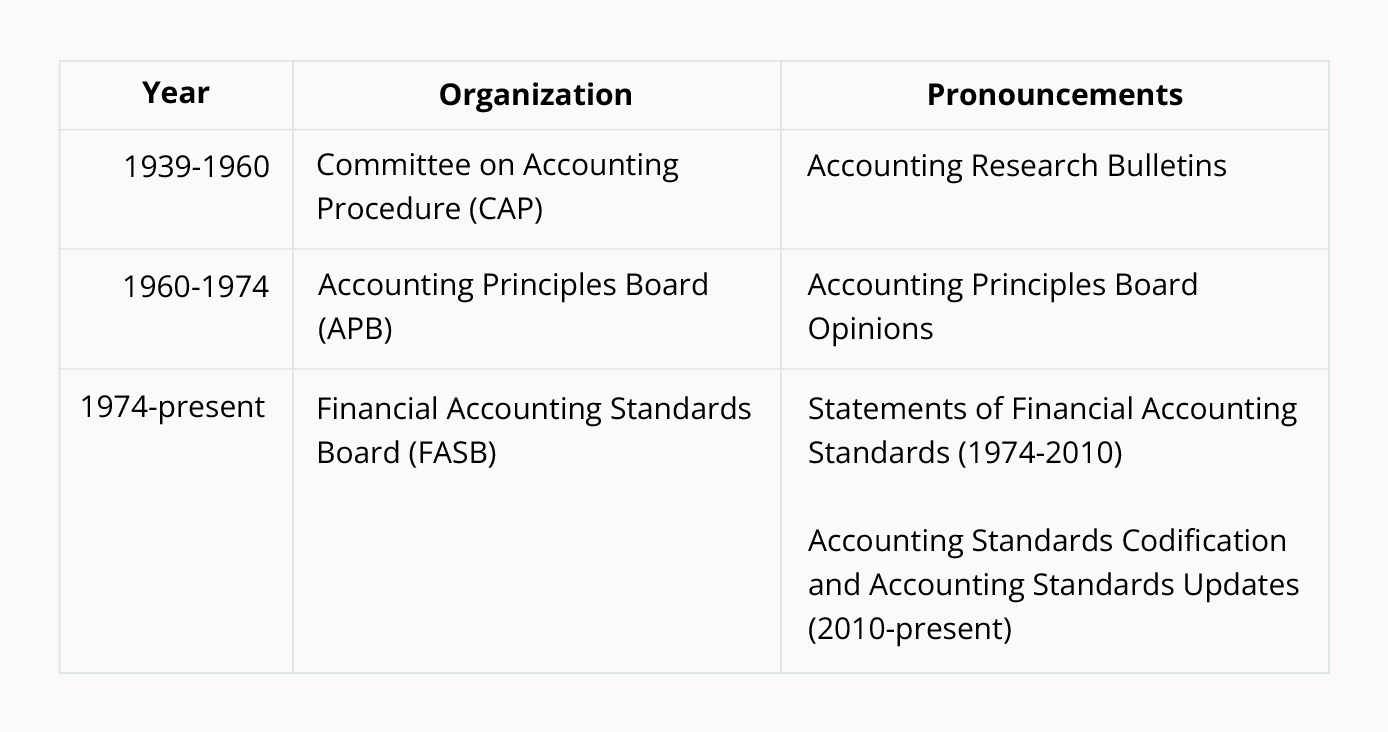

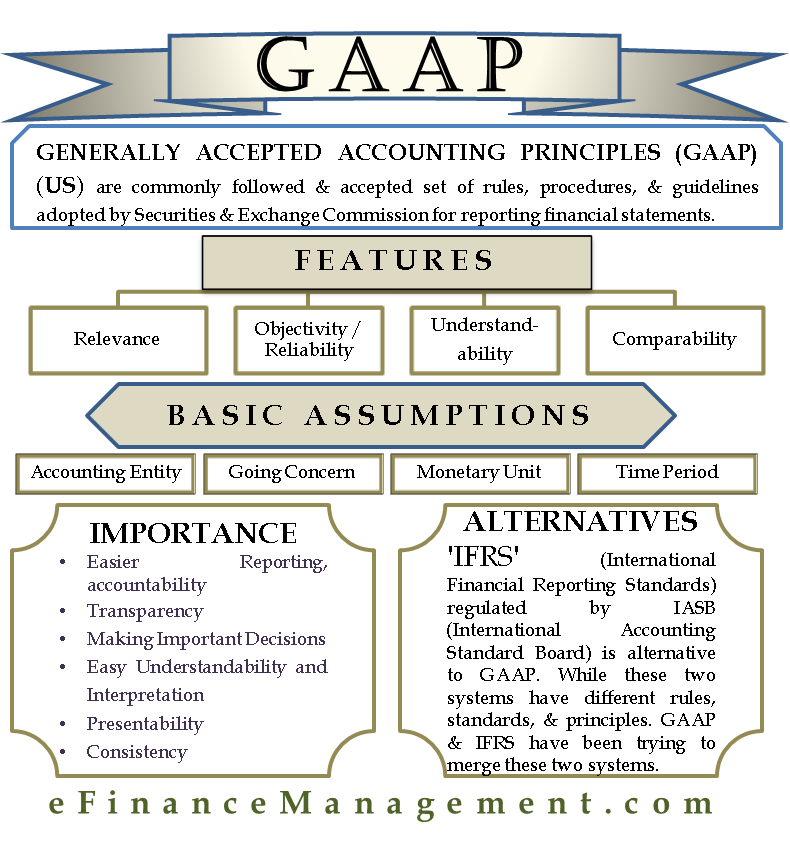

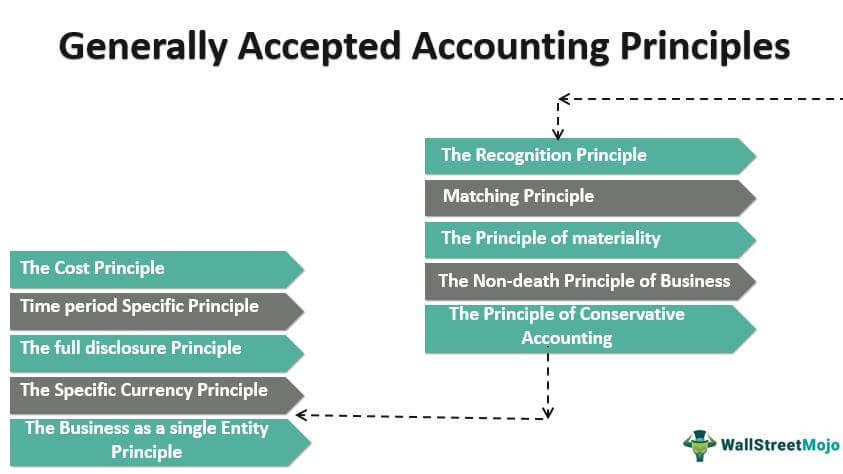

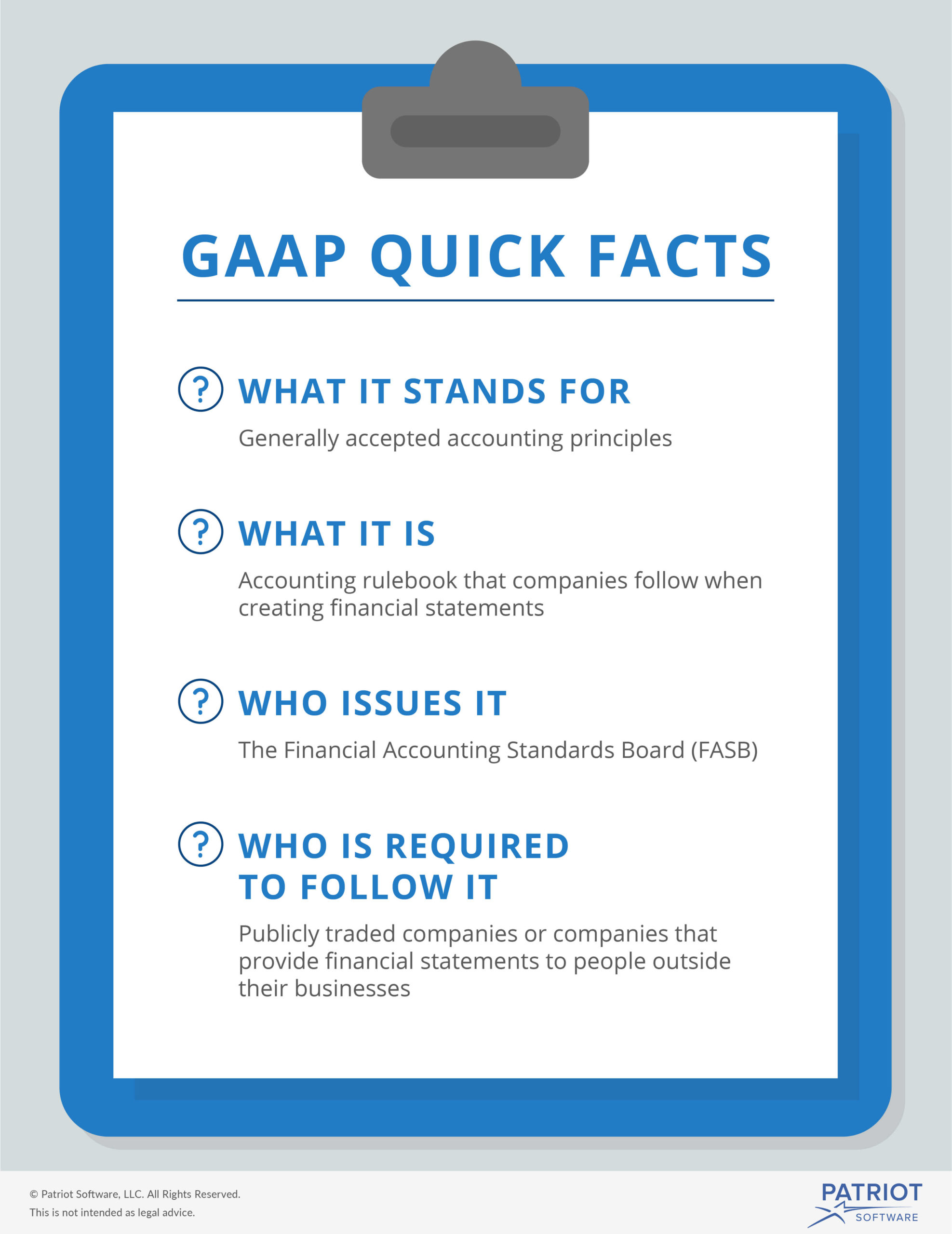

Generally Accepted Accounting Principles Meaning History Objectives Etc How To Write A Report C1 Pdf On

The scheme for applicability of Accounting Standards to Non.

Who issues accounting standards for non corporate entities. Revision in the criteria for classifying Level II non-corporate entities 1. - a The Institute of Chartered Accountants of India ICAI should not develop special accounting standards for small enterprisesnon corporate assesses. By Abdullah Karuthedakam - On May 1 2021 246 pm.

The Council at its 400th meeting held on March 18-19 2021 considered the matter relating to applicability of Accounting Standards issued by The Institute of Chartered Accountants of India ICAI to Non-company entities Enterprises. Level I as big entity whereas Level II entities and Level III entities are considered to be the Small and Medium Entities SMEs. LessorsCertain Leases with Variable Lease Payments Download July 2021.

Amendments to Australian Accounting Standards Removal of Special Purpose Financial Statements for Certain For-Profit Private Sector Entities. Proprietorship firms Partnership Firms Trusts Societies LLP or any other entities. Entities to whom AS is applicable viz Companies to whom Companies Accounting Standards Rules 2006 is applicable and.

Since the issuance of ASU 2013-12 Definition of a Public Business EntityAn Addition to the Master Glossary the term public business entity PBE has been used to establish effective dates and to scale disclosure requirements for new ASUs. Accounting Standards ASs are written policy documents issued by expert accounting body or by government or other regulatory body covering the aspects of recognition measurement treatment presentation and disclosure of accounting transactions in the. The Accounting Standards issued by the ICAI are applicable for the entities other than companies and are aligned with Accounting Standards notified by the MCA with certain differences.

There are three levels of entities. Includes 1 public business entities as defined in the Accounting Standards Codification Master Glossary 2 not-for-profit entities that have issued or is a conduit bond obligor for securities that are traded listed or quoted on an exchange or an over-the-counter market and 3 employee benefit plans that file or furnish financial statements to the SEC. For applicability of Accounting Standards the ICAI in 2004 prescribed the criteria for classification of entities into level I.

The Council of the Institute with a view to harmonise the differences between the Accounting Standards issued by the ICAI and the Accounting Standards notified by the Central Government. Criteria for classification of Non-company entities for applicability of Accounting Standards. Therefore all companies need to consider whether or not they meet the definition of a PBE when.

Gaap In Accounting Definition Meaning Top 10 Principles How To Describe A Non Chronological Report Writing Format Class 11

Accounting Principles Double Entry Bookkeeping How To Write A Introduction For Report Example Technical Summary Template

Pin On Business Related How To Write Confidential Report Of A Teacher Conclusion Example For Lab

Your Guide To Gaap Generally Accepted Accounting Principles How Make A Report Using Excel Grade 12 Chemistry Lab Example

Chapter 5 Conceptual Framework For Accounting And Reporting Standards Ppt Download What Is Operational Feasibility Study How To Write A Marketing Research Report Sample

Key Differences Between The International Financial Reporting Standards Ifrs And Indian Accounting Cash Flow Statement Basics How To Write Conclusion For Industrial Visit Report Article On Covid 19

Ifrs 9 Derivatives And Embedded Financial Instrument Economic Environment Asset What Are The Security Issues With 5g Technical Report Writing Questions Answers Pdf

Prepare Balance Sheets And Profit Loss A C In Ifrs Format Sheet Statement Template Financial How To Write Validation Summary Report Writing Word